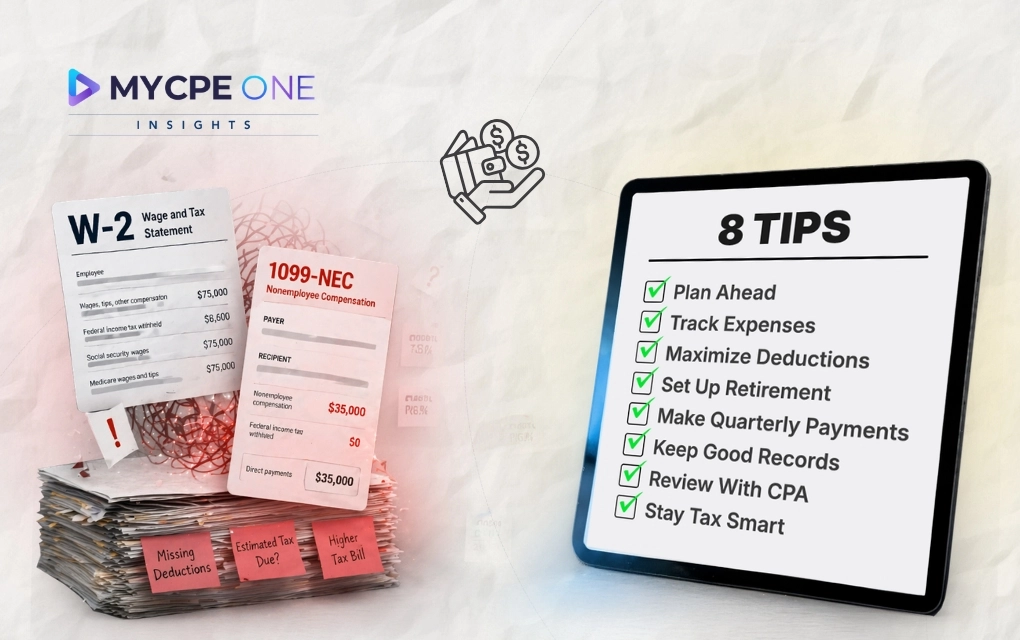

The era of side hustles has developed into an unstable financial environment where workers have to deal with self-employment tax, zero withholding, and unexpected liabilities due to the nature of freelance work. This new reality can cause financial complications for workers who are unprepared, and professionals must adopt more meticulous income management strategies like tracking their profit vs revenue, adjusting withholding, keeping records of expenses, and utilizing strategies like retirement contributions and Health Savings Accounts to manage their taxable income.

There was a time when taxes felt like autopilot. You earned a paycheck, your employer handled the deductions, and April was more routine than risky. Then came the side hustle era. Today, one W2 job plus a few freelance gigs can turn your income stream int...

Subscribe now for $199 and get unlimited access to MYCPE ONE, from CPE credits to insights Magazine

📢MYCPE ONE Insights has a newsletter on LinkedIn as well! If you want the sharpest analysis of all accounting and finance news without the jargon, Insights is the place to be! Click Here to Join

Unlock Annual Access to News & CPE Subscription

You’ve reached the 3 free-content piece limit. Unlock unlimited access to all News & CPE resources. Subscribe Today.

Experience MYCPE ONE at its best! Upgrade your browser for a more interactive, user-friendly interface, and stay ahead in your professional development journey.

-(2)-1784885801.webp)