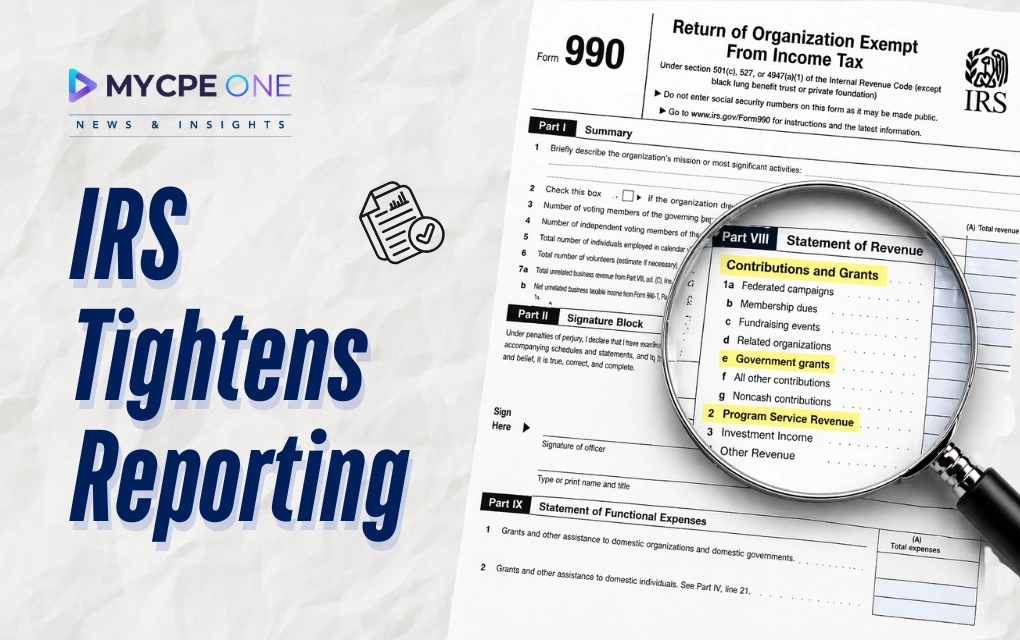

It used to be that Form 990 was a quiet compliance exercise. File it, archive it, move on. Now it is starting to look less like paperwork and more like a spotlight. And not the soft kind. The IRS just turned the dial up. Between a planned overhaul of Form...