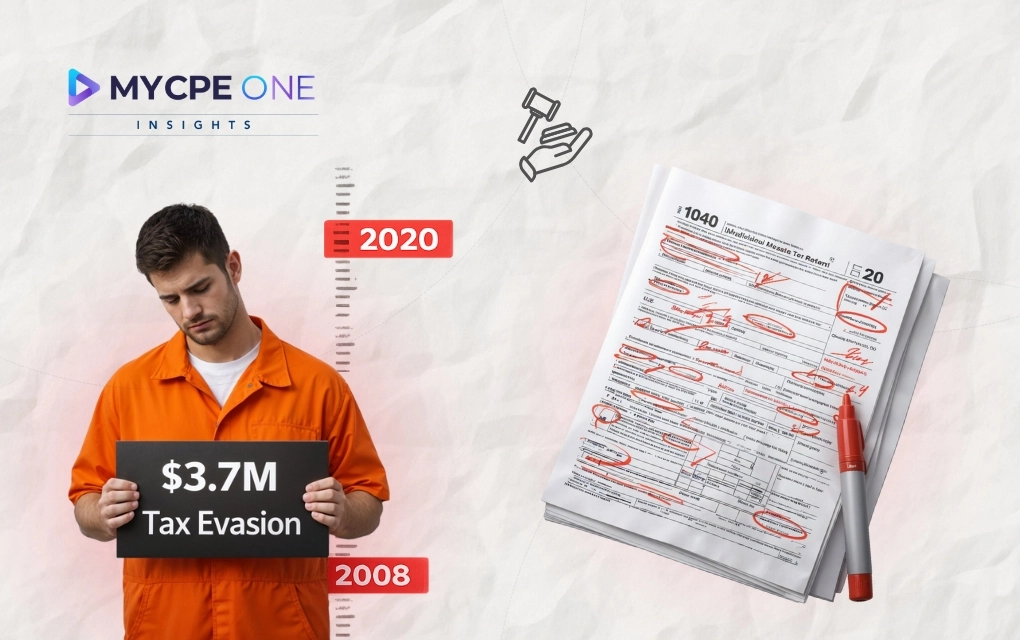

Phillip Mak, a businessman from Jacksonville, pleaded guilty to attempted tax evasion after not paying federal income tax on more than $10 million he earned between 2008 and 2020, and then attempting to move money and assets out of government reach. The case highlights the consequences of tax non-compliance, criminal activity, and underlines the importance of understanding the implications of financial decisions made during active IRS collection.

Earning more than $10 million and paying zero federal income tax for over a decade is not a paperwork oops. It is a ticking clock. That clock finally ran out for Phillip Mak, a Jacksonville-area businessman who pleaded guilty to attempted tax evasion...

Subscribe now for $199 and get unlimited access to MYCPE ONE, from CPE credits to insights Magazine

📢MYCPE ONE Insights has a newsletter on LinkedIn as well! If you want the sharpest analysis of all accounting and finance news without the jargon, Insights is the place to be! Click Here to Join

Unlock Annual Access to News & CPE Subscription

You’ve reached the 3 free-content piece limit. Unlock unlimited access to all News & CPE resources. Subscribe Today.

Experience MYCPE ONE at its best! Upgrade your browser for a more interactive, user-friendly interface, and stay ahead in your professional development journey.

-1783514395.webp)