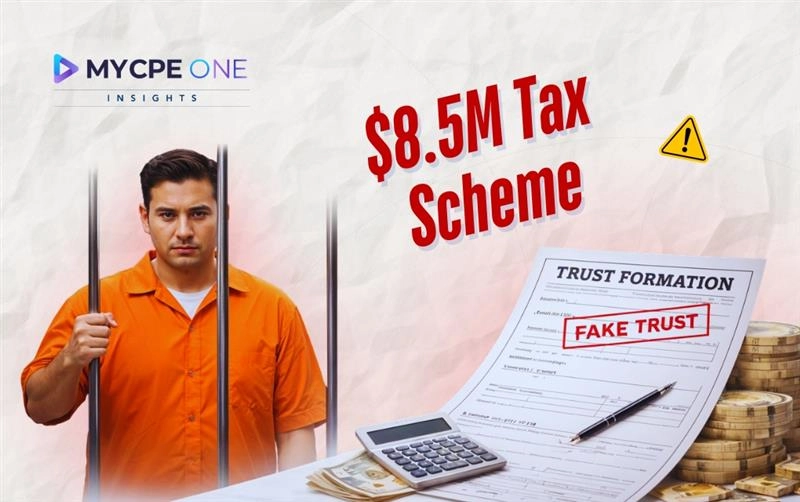

Most tax fraud cases don’t start with flashy schemes or complex loopholes. They start with something much simpler, a belief that the system can be bent just enough to go unnoticed. Sometimes it’s a small misreporting. Sometimes it’s aggressive structuring...

-1785503494.webp)