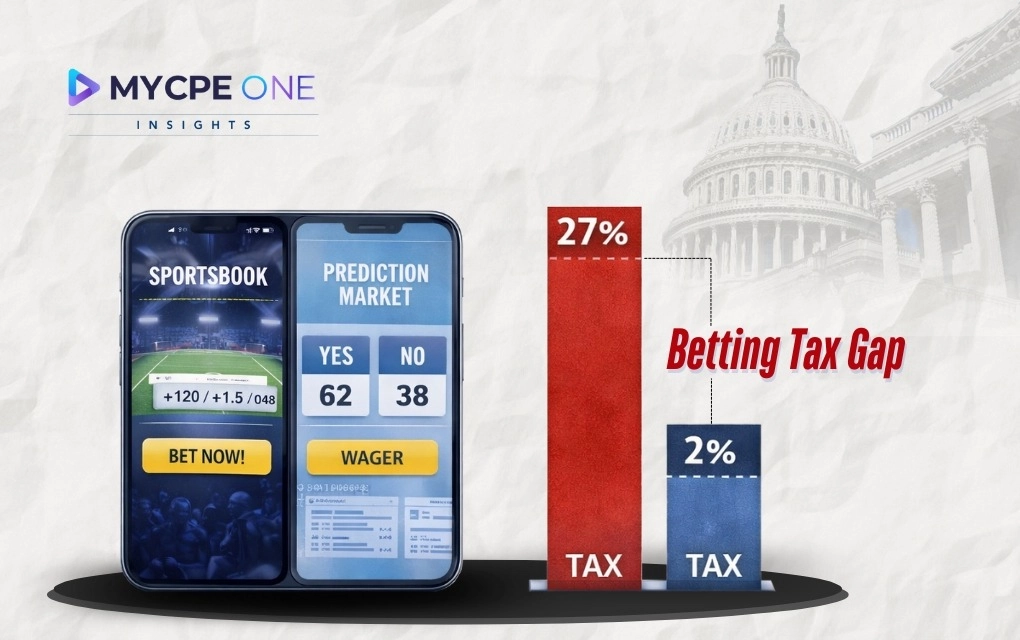

Picture two friends placing the same Super Bowl wager. One taps the app on FanDuel in New York. The other places a near-identical contract on Kalshi from the same couch. Same bet, same risk, same outcome. Yet the tax trail behind those two taps looks comp...

-1785503494.webp)