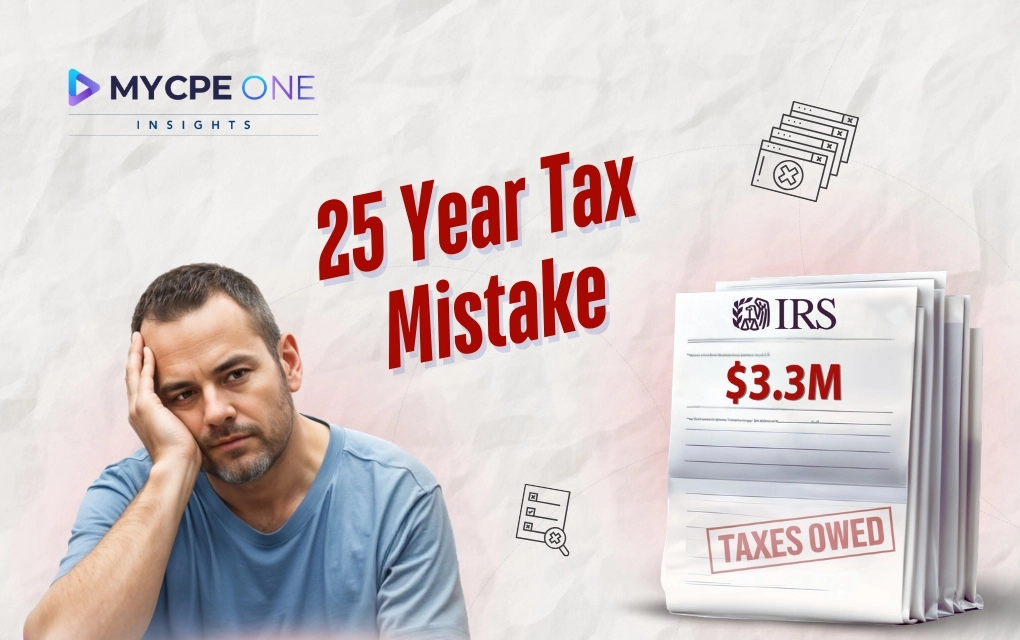

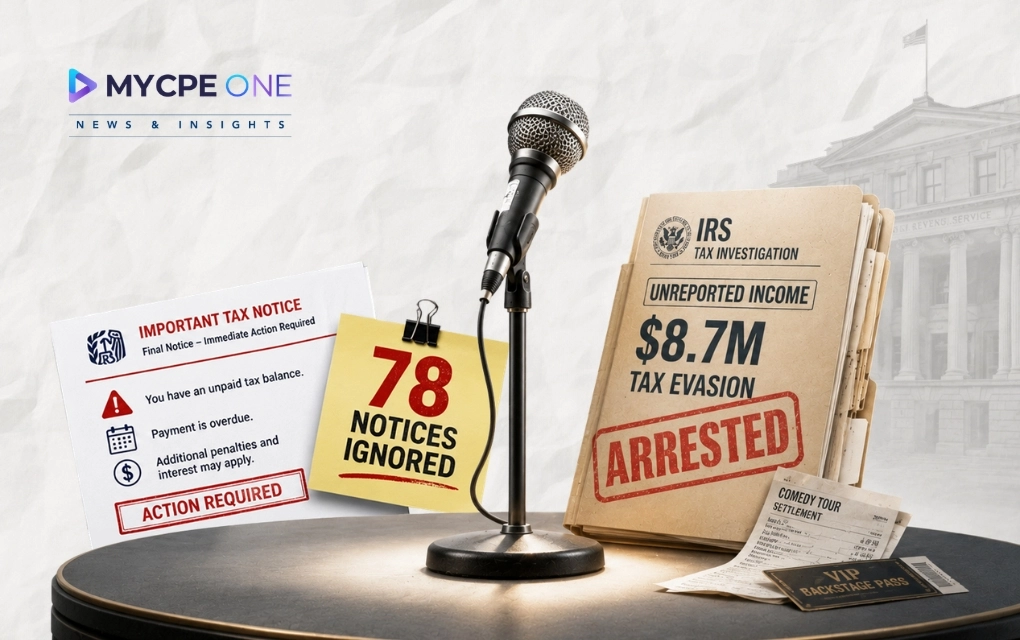

Richard Hatch, the first-ever winner of Survivor in 2000, is facing a $3.3 million tax liability on the $1 million prize money that he won on the show. Hatch, who was already convicted in 2006 for filing false tax returns and served 51 months in prison, failed to comply fully with the amended returns for 2000 and 2001 and now faces additional taxes, interest, and penalties.

He won a million bucks on national TV, walked off an island, and into a 26-year tax problem. If that sounds like the kind of story you’d expect to wrap up in a clean IRS notice and a payment plan, think again. Richard Hatch, the first-ever winner of Survi...

Subscribe now for $199 and get unlimited access to MYCPE ONE, from CPE credits to insights Magazine

📢MYCPE ONE Insights has a newsletter on LinkedIn as well! If you want the sharpest analysis of all accounting and finance news without the jargon, Insights is the place to be! Click Here to Join

Unlock Annual Access to News & CPE Subscription

You’ve reached the 3 free-content piece limit. Unlock unlimited access to all News & CPE resources. Subscribe Today.

Experience MYCPE ONE at its best! Upgrade your browser for a more interactive, user-friendly interface, and stay ahead in your professional development journey.