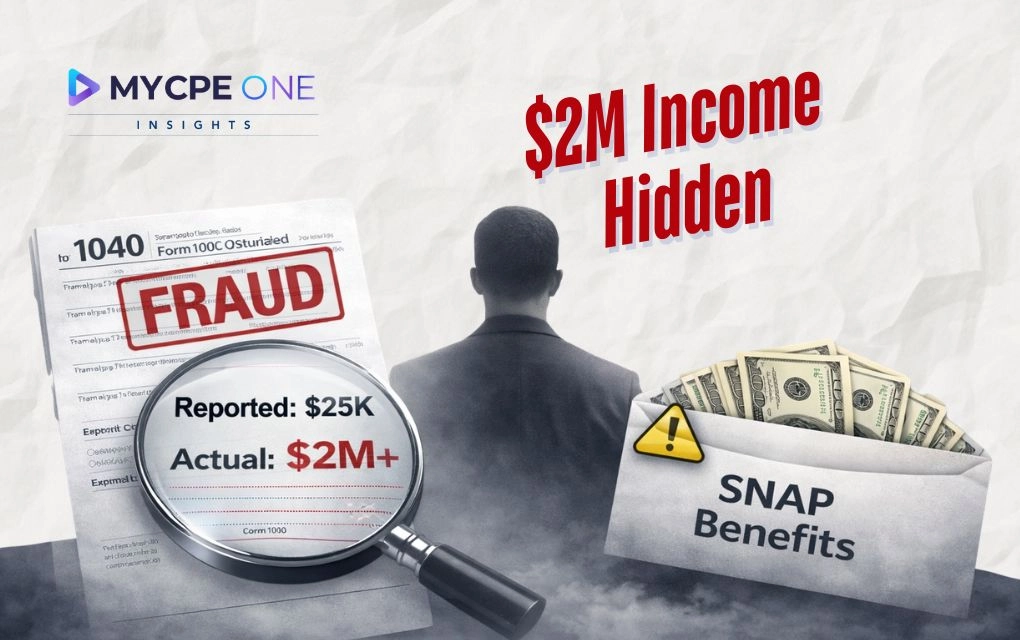

A Minnesota man is accused of tax fraud, underreporting nearly $2 million in income, avoiding over $186,000 in taxes, whilst simultaneously collecting around $40,000 in benefits intended for low-income households. This case exemplifies the increasing sophistication of tax enforcement mechanisms that connect data from different systems to identify inconsistencies and fraud, and it serves as a stark warning for professionals about the penalties of tax evasion and fraud.

Every tax season has that one story professionals quietly talk about, the client who thought they could stay one step ahead of the system. It usually starts small. A number adjusted here, an expense stretched there. Then it compounds. One year becomes fou...

Subscribe now for $199 and get unlimited access to MYCPE ONE, from CPE credits to insights Magazine

📢MYCPE ONE Insights has a newsletter on LinkedIn as well! If you want the sharpest analysis of all accounting and finance news without the jargon, Insights is the place to be! Click Here to Join

Unlock Annual Access to News & CPE Subscription

You’ve reached the 3 free-content piece limit. Unlock unlimited access to all News & CPE resources. Subscribe Today.

Experience MYCPE ONE at its best! Upgrade your browser for a more interactive, user-friendly interface, and stay ahead in your professional development journey.

-1785503494.webp)