Picture this. You finally explain to a client that their tips are tax-free. They smile, maybe even call you a genius. Then you add, “Well… federally.” Cue the blank stare. Welcome to 2026, where the tax code feels less like a rulebook a...

Join 250,000+

professionals today

Add Insights to your inbox - get the latest

professional news for free.

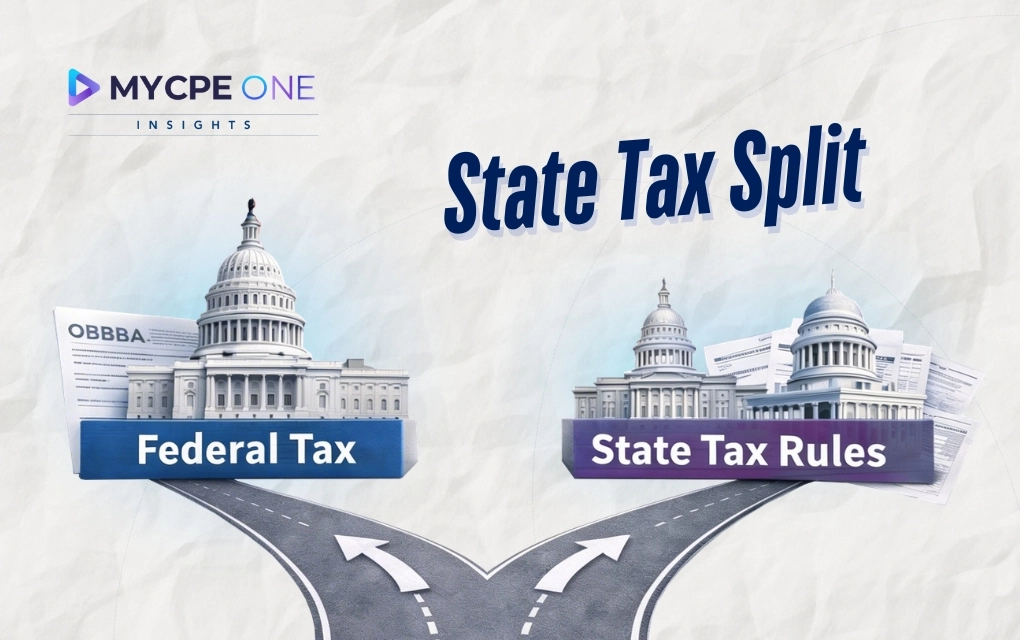

Why States Are Quietly ‘Decoupling’ from OBBBA

Join our 250K+ subscribers

Join our 250K+ subscribers

Subscribe17 MAR 2026 / ACCOUNTING & TAXES

The One Big Beautiful Bill Act passed in 2025 federally provides generous tax relief, including full exemption on tips and overtime. Nonetheless, numerous states have diverged from this tax code according to their individual budget needs, effectively creating a fragmented patchwork of taxation that leaves taxpayers and their advisors in complicated territory.

Picture this. You finally explain to a client that their tips are tax-free. They smile, maybe even call you a genius. Then you add, “Well… federally.” Cue the blank stare. Welcome to 2026, where the tax code feels less like a rulebook a...

Until next time…

Don’t forget to share this story on LinkedIn, X and Facebook

Subscribe now for $199 and get unlimited access to MYCPE ONE, from CPE credits to insights Magazine

📢MYCPE ONE Insights has a newsletter on LinkedIn as well! If you want the sharpest analysis of all accounting and finance news without the jargon, Insights is the place to be! Click Here to Join

You’ve reached the 3 free-content piece limit. Unlock unlimited access to all News & CPE resources.

Subscribe Today.

Already have an account?

Sign In

-1785503494.webp)