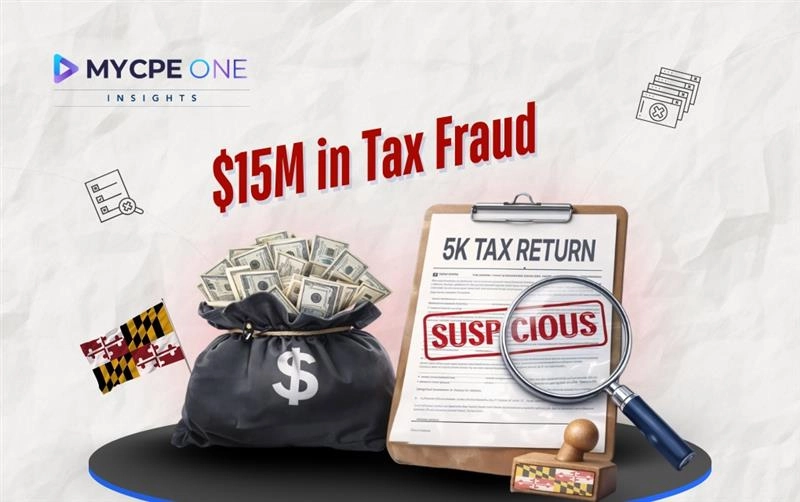

Maryland authorities recently blocked over $15 million in fraudulent tax refunds, flagging more than 5,000 suspicious returns ahead of the annual deadline. This represents a rapidly growing trend of sophisticated, tech-driven tax fraud schemes involving identity theft, false filings, phishing, and misuse of tax credits, necessitating increased use of advanced analytics and artificial intelligence for fraud detection, as well as stricter verification processes and early filing by taxpayers.

A taxpayer files early, expecting a smooth refund. Weeks later, a notice arrives asking them to verify their identity. Confusion sets in, they already filed, so what changed? In many cases, the answer is simple and unsettling: someone else filed first. It...

Subscribe now for $199 and get unlimited access to MYCPE ONE, from CPE credits to insights Magazine

📢MYCPE ONE Insights has a newsletter on LinkedIn as well! If you want the sharpest analysis of all accounting and finance news without the jargon, Insights is the place to be! Click Here to Join

Unlock Annual Access to News & CPE Subscription

You’ve reached the 3 free-content piece limit. Unlock unlimited access to all News & CPE resources. Subscribe Today.

Experience MYCPE ONE at its best! Upgrade your browser for a more interactive, user-friendly interface, and stay ahead in your professional development journey.