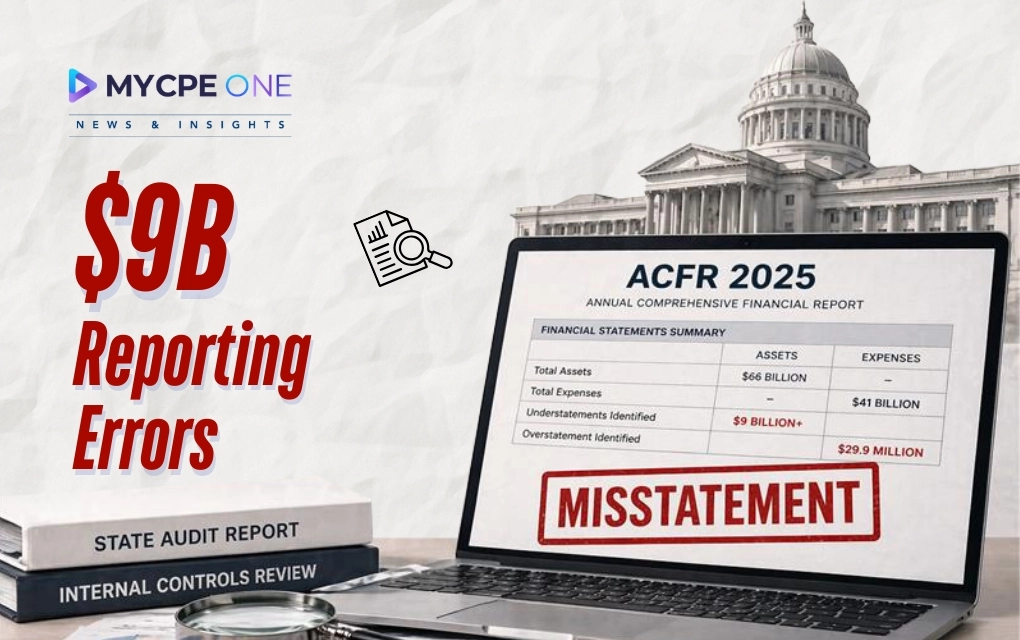

Somewhere between a late-night Excel session and a “we’ll fix it in review” mindset, Missouri’s financial statements picked up a $9 billion problem. Not fraud. Not missing cash. Just good old-fashioned human error, scaled up to num...

Join 250,000+

professionals today

Add Insights to your inbox - get the latest

professional news for free.

Missouri Audit Reveals $9B in Financial Reporting Errors

Join our 250K+ subscribers

Join our 250K+ subscribers

Subscribe21 APR 2026 / BUSINESS

CPE Approved

Missouri's financial statements encountered a $9 billion issue due to human error and lack of proper audit controls, causing discrepancies in fiduciary funds—primarily tied to retirement system investments. The issue highlights the importance of reliable internal control systems, prompts concerns about public trust and federal funding, and underscores the need for automation in financial processes to prevent similar problems in the future.

Somewhere between a late-night Excel session and a “we’ll fix it in review” mindset, Missouri’s financial statements picked up a $9 billion problem. Not fraud. Not missing cash. Just good old-fashioned human error, scaled up to num...

Until next time…

Don’t forget to share this story on LinkedIn, X and Facebook

Subscribe now for $199 and get unlimited access to MYCPE ONE, from CPE credits to insights Magazine

📢MYCPE ONE Insights has a newsletter on LinkedIn as well! If you want the sharpest analysis of all accounting and finance news without the jargon, Insights is the place to be! Click Here to Join

You’ve reached the 3 free-content piece limit. Unlock unlimited access to all News & CPE resources.

Subscribe Today.

Already have an account?

Sign In-(1)-1785429054.webp)