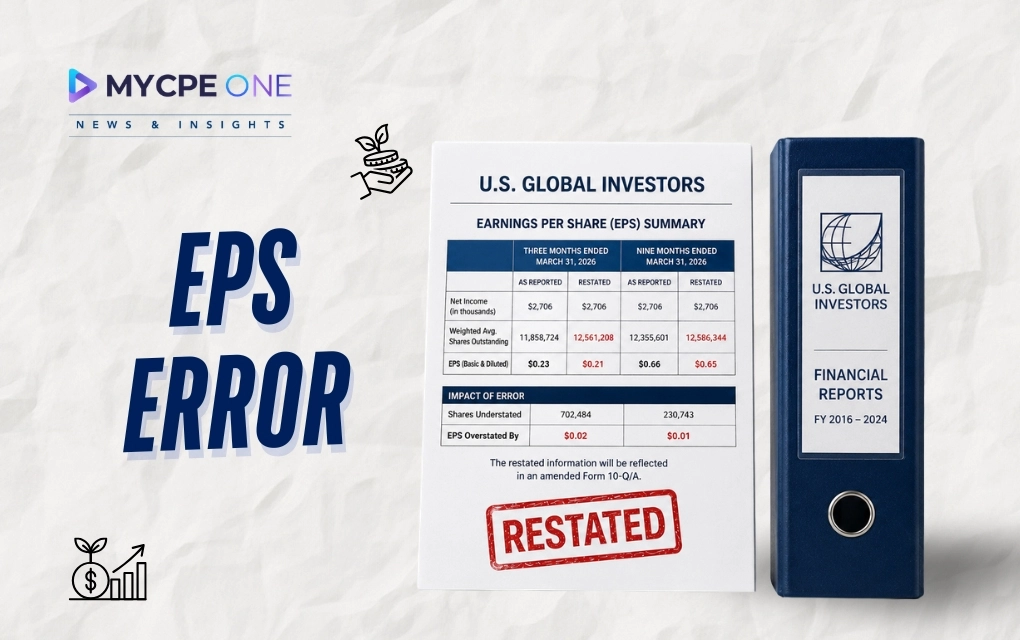

Accounting mistakes often hide in spreadsheets rather than appearing as obvious problems. That was the case for U.S. Global Investors, Inc. (NASDAQ: GROW), which announced a restatement of its earnings per share (EPS) figures for the three- and nine-...

-(1)-1785429054.webp)