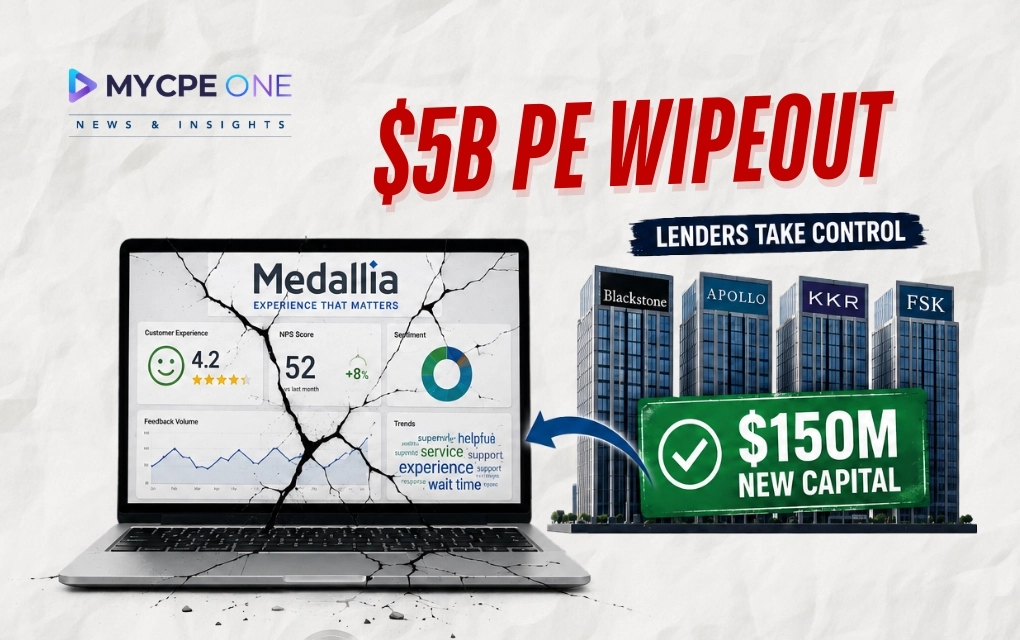

Private equity firm Thoma Bravo has handed over software firm Medallia to a lender group led by Blackstone, Apollo, KKR, and FSK following a failed deal model and growing debt; Thoma Bravo lost approximately $5 billion of equity from its 2021 takeover. The new owners plan to inject $150 million and reduce the company's debt, with Medallia's strategic focus now pivoting towards developing AI-driven tools to enhance customer and employee feedback analysis.

In private equity, the spreadsheet usually looks polite before the bill shows up. Medallia’s story is one of those deals that probably looked clean in the 2021 model: sticky enterprise software, a big customer experience market, recurring revenue, a tech...

Subscribe now for $199 and get unlimited access to MYCPE ONE, from CPE credits to insights Magazine

📢MYCPE ONE Insights has a newsletter on LinkedIn as well! If you want the sharpest analysis of all accounting and finance news without the jargon, Insights is the place to be! Click Here to Join

Unlock Annual Access to News & CPE Subscription

You’ve reached the 3 free-content piece limit. Unlock unlimited access to all News & CPE resources. Subscribe Today.

Experience MYCPE ONE at its best! Upgrade your browser for a more interactive, user-friendly interface, and stay ahead in your professional development journey.