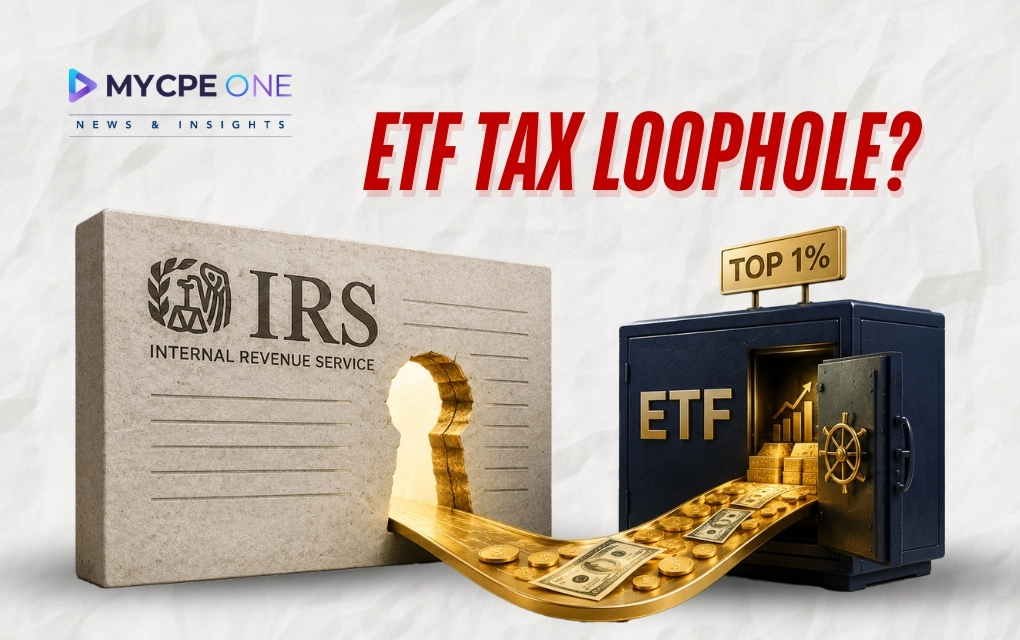

Tax strategists in the US have been utilising lesser-known tax breaks and loopholes related to ETFs, 351 conversions, qualified small business stock, stepped up basis, and the wider tax gap tied to pass-through income, provoking bigger questions about the sustainability of these tax planning methods. The ETF tax break, for example, is estimated to cost the US Treasury around $48 billion a year, with the top 1% of households receiving approximately 39.6% of this benefit. This use of legal deferrals and avoidances is increasingly causing concerns about significant revenue drain, prompting scrutiny from lawmakers, the Treasury, and the IRS.

A tax loophole rarely walks into the room wearing a name tag. It usually shows up in the fine print, sits quietly for years, and then one day someone in wealth management figures out how to turn it into real money. That is roughly where the U.S. tax...

Subscribe now for $199 and get unlimited access to MYCPE ONE, from CPE credits to insights Magazine

📢MYCPE ONE Insights has a newsletter on LinkedIn as well! If you want the sharpest analysis of all accounting and finance news without the jargon, Insights is the place to be! Click Here to Join

Unlock Annual Access to News & CPE Subscription

You’ve reached the 3 free-content piece limit. Unlock unlimited access to all News & CPE resources. Subscribe Today.

Experience MYCPE ONE at its best! Upgrade your browser for a more interactive, user-friendly interface, and stay ahead in your professional development journey.