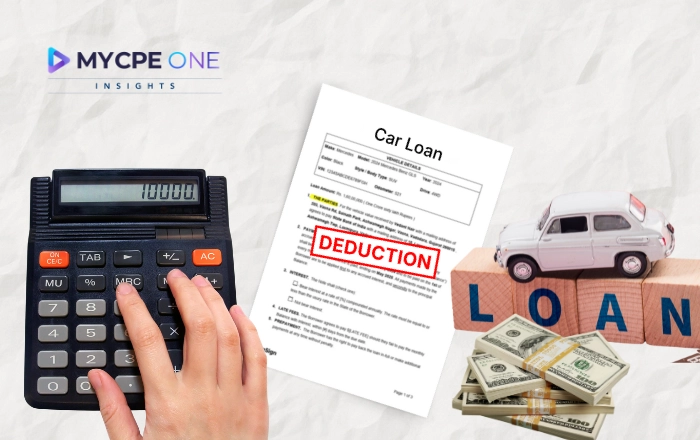

Washington just tossed drivers a headline that sounds like a pit crew miracle: “no tax on car loan interest.” Starting in tax year 2025, the One Big Beautiful Bill Act (OBBBA) lets eligible taxpayers deduct up to $10,000 a year in interest on a ...

Join 250,000+

professionals today

Add Insights to your inbox - get the latest

professional news for free.

Is the New Car Loan Tax Break Real or Just Smoke?

Join our 250K+ subscribers

Join our 250K+ subscribers

Subscribe22 DEC 2025 / ACCOUNTING & TAXES

The US government has introduced the One Big Beautiful Bill Act (OBBBA) which allows certain taxpayers to deduct up to $10,000 a year in interest on qualified car loans from 2025-2028. The policy appears to be a strategic incentive to encourage the purchase of new vehicles assembled domestically, but is in truth limited by strict eligibility criteria that includes specific income limits and loan conditions.

Washington just tossed drivers a headline that sounds like a pit crew miracle: “no tax on car loan interest.” Starting in tax year 2025, the One Big Beautiful Bill Act (OBBBA) lets eligible taxpayers deduct up to $10,000 a year in interest on a ...

Until next time…

Don’t forget to share this story on LinkedIn, X and Facebook

Subscribe now for $199 and get unlimited access to MYCPE ONE, from CPE credits to insights Magazine

📢MYCPE ONE Insights has a newsletter on LinkedIn as well! If you want the sharpest analysis of all accounting and finance news without the jargon, Insights is the place to be! Click Here to Join

The Only All-in-One CPE & Learning Platform for CPA & Accounting Firms

Get everything you need for team learning and CPE compliance-starting at just $199 per user/year!

You’ve reached the 3 free-content piece limit. Unlock unlimited access to all News & CPE resources.

Subscribe Today.

Already have an account?

Sign In

-1785503494.webp)