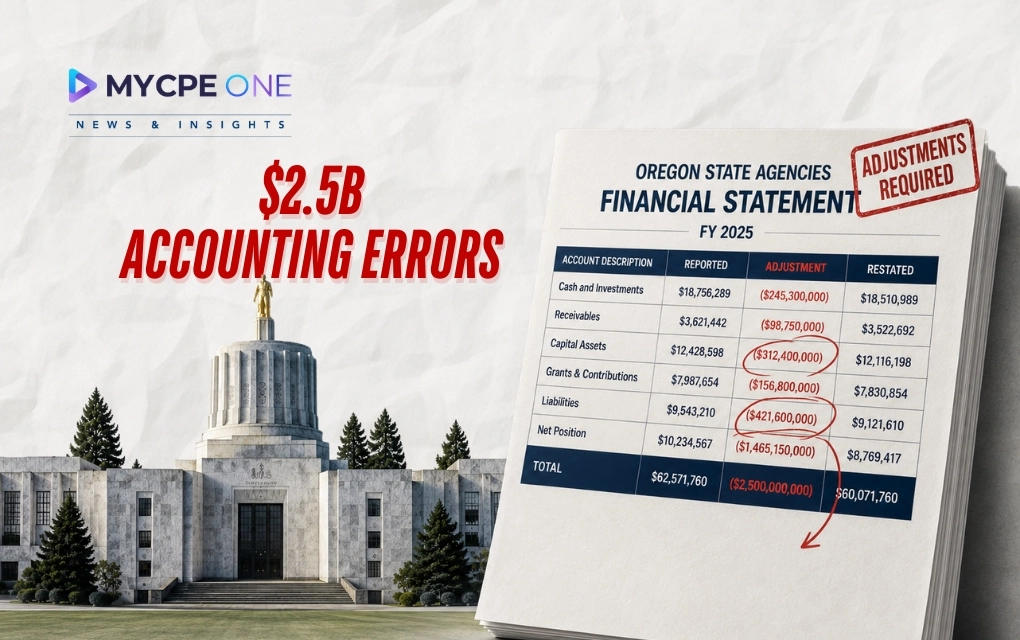

Ever reconcile an account and discover the numbers eventually balance, but only after three hours, four spreadsheets, and a strong cup of coffee? Oregon’s latest audit feels a bit like that. The state received a clean audit opinion for fiscal year 2025, m...

-1785944450.webp)