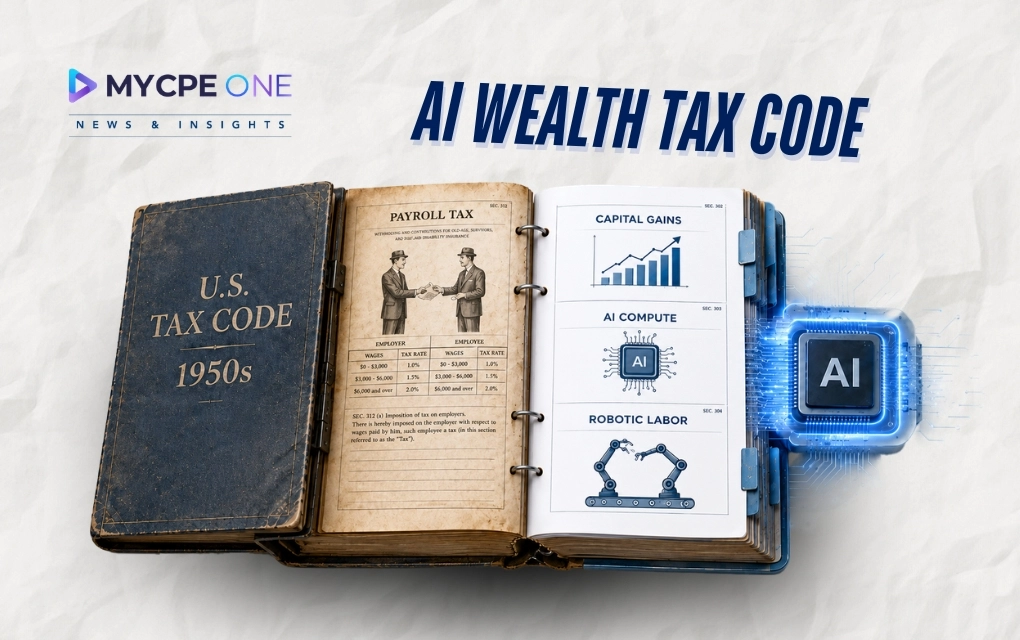

AI is taking on tasks traditionally performed by humans, prompting debates over how to tax the resulting economic value. Some argue for direct tax on AI operations such as data centers, while others favor reforming capital income tax. This shift could challenge the traditional US tax model, which relies substantially on human labour, and raises questions about future government revenue sources in an increasingly automated economy.

AI has started to look less like a shiny tool and more like a very expensive intern who never sleeps, never asks for benefits, and somehow knows how to write code, draft memos, summarize contracts, and build a model before lunch. That sounds great until t...

Subscribe now for $199 and get unlimited access to MYCPE ONE, from CPE credits to insights Magazine

📢MYCPE ONE Insights has a newsletter on LinkedIn as well! If you want the sharpest analysis of all accounting and finance news without the jargon, Insights is the place to be! Click Here to Join

Unlock Annual Access to News & CPE Subscription

You’ve reached the 3 free-content piece limit. Unlock unlimited access to all News & CPE resources. Subscribe Today.

Experience MYCPE ONE at its best! Upgrade your browser for a more interactive, user-friendly interface, and stay ahead in your professional development journey.

-1784727396.webp)

-1784280137.webp)